Tuesday, July 17, 2012

“…a money supply based on nothing other than faith in government is a productivity killer.”

John Aziz is a young British blogger on matters economic, publishing at azizonomics: economics for the jilted generation. In a recent entry he addresses the predicament that during the post-war gold-exchange standard “average family income increased at a greater rate than that of the top 1%. From 1979-2007 (years without a gold standard) the top 1% did much, much better than the average family.” The stagnation of family income, and the growing disparity between the middle class and the wealthy is, of course, one of the fundamental complaints underlying the former Occupy Wall Street movement and its more structured successor, the 99% Spring. Of course, economic growth rates are a combination of labor force growth plus productivity growth. Without productivity growth wages stagnate. So … consider the correlation between monetary policy and productivity growth (and the absence thereof).

Aziz writes, with exceptional lucidity:

I have long suspected that a money supply based on nothing other than faith in government is a productivity killer.

Last November I wrote:

As we have seen with the quantitative easing program, the newly-printed money is directed to the rich. The Keynesian response to that might be that income growth inequality can be solved (or at least remedied) by making sure that helicopter drops of new money are done over the entire economy rather than directed solely to Wall Street megabanks.

But I think there is a deeper problem here. My hypothesis is that leaving the gold exchange standard was a free lunch: GDP growth could be achieved without any real gains in productivity, or efficiency, or in infrastructure, but instead by just pumping money into the system.

And now I have empirical evidence that my hypothesis has been true — total factor productivity.

In 2009 the Economist explained TFP as follows:

Productivity growth is perhaps the single most important gauge of an economy’s health. Nothing matters more for long-term living standards than improvements in the efficiency with which an economy combines capital and labour. Unfortunately, productivity growth is itself often inefficiently measured. Most analysts focus on labour productivity, which is usually calculated by dividing total output by the number of workers, or the number of hours worked.

A better gauge of an economy’s use of resources is “total factor productivity” (TFP), which tries to assess the efficiency with which both capital and labour are used.

Total factor productivity is calculated as the percentage increase in output that is not accounted for by changes in the volume of inputs of capital and labour. So if the capital stock and the workforce both rise by 2% and output rises by 3%, TFP goes up by 1%.

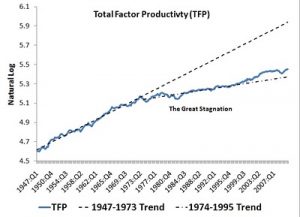

Here’s US total factor productivity:

Only a willful and ideological Keynesian could ignore the salient detail: as soon as the USA left the gold exchange standard, total factor productivity began to dramatically stagnate.

Coincidence? I don’t think so — a fundamental change in the nature of the money supply coincided almost exactly with a fundamental change to the shape of the nation’s economy. Is the simultaneous outgrowth in income inequality a coincidence too?

And it’s not just total factor productivity that has been lower than in the years when America was on the gold exchange standard — as a Bank of England report recently found, GDP growth has averaged lower in the pure fiat money era (2.8% vs 1.8%), and financial crises have been more frequent in the non-gold-standard years.

The authors of the report noted:

Overall the gold standard appeared to perform reasonably well against its financial stability and allocative efficiency objectives.

Still think it’s a barbarous relic?

Full marks, Mr. Aziz.

Recent Comments